Researchers from the XRP community recently turned their attention to an outdated statement from investment banking giant Morgan Stanley.

This rating was highlighted by @SMQKEDQG and was published in an academic review from the Boston University Banking and Financial Law Review (Vol. 36). In particular, Morgan Stanley’s original perception appeared in a publication entitled “Bank Blockchain: A Destructive Threat or Tool?”

Advance faster, safer, cheaper passes

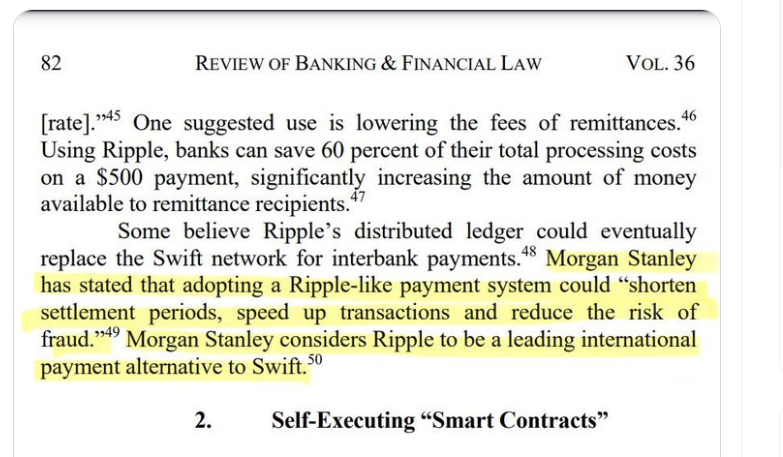

According to the Journal, Morgan Stanley noted that adopting a “ripple-like payment system” can reduce payment times, accelerate transactions and reduce the risk of fraud. These enhancements cover years of inefficiency in cross-border banking. This bank often slows down transactions with delays, intermediaries and costly forex conversions.

Ripple’s distributed ledger technology (DLT) enables real-time transaction processing without the need for a correspondent’s bank account. This solution dramatically reduces bank operating costs and increases the amount of funds available to remit customers.

This article ripples among the most serious candidates to overhaul an outdated banking infrastructure, especially when cited alongside a wider use case for blockchain in the financial sector. From smart contracts to improved compliance, the legal review points to DLT, particularly ripple as a much-needed tool of change.

In addition to Ripple, this work explores how Ethereum’s smart contracts and blockchain-based audit trails can increase regulatory oversight and transparency.

Morgan Stanley Recognizing ripples

Increased legitimacy of interagency Ripple

Morgan Stanley’s quote shows the growing institutional awareness of Ripple’s model as a viable alternative to legacy systems. In particular, this perception is not new. Previously, jpmorgan Highlighted XRP and Ripple are key players in unlocking $120 billion locked in inefficient cross-border payments.

It noted that the multinationals have transferred $23.5 trillion per year, or about 25% of the world’s GDP. However, these funds face significant inefficiencies in speed, cost and transparency. These issues generate annual transaction costs of $120 billion due to forex conversion, trapped liquidity, and delayed settlements.

While entities like Ripple, Swift and CLS Group are working on solutions, JPMorgan noted that Swift still relies on an outdated correspondent banking system, and that CLS Group only supports 18 currencies.

Meanwhile, Ripple’s real-time payment infrastructure has realised that it may be using XRP for settlements but criticised cryptocurrency volatility.

In particular, there is the ripple itself It was published You are developing a system that acts as an alternative to Swift. However, it is still unclear whether Ripple will eventually replace Swift.

Despite the uncertainty, when companies like Morgan Stanley publicly acknowledge Ripple’s potential, it adds weight to the aspirations of XRP enthusiasts.