Santiago Roel Santos, founder and CEO of venture capital firm Inversion Capital, said financial platforms are rushing to add prediction markets at the cost of accelerating “casino-like” user churn.

In a blog post on Saturday, Santos claimed that while he “believes in the fundamental tenets” of prediction markets, he believes offering them on mainstream financial apps like Robinhood increases the risk of liquidation of user accounts and threatens future value capture.

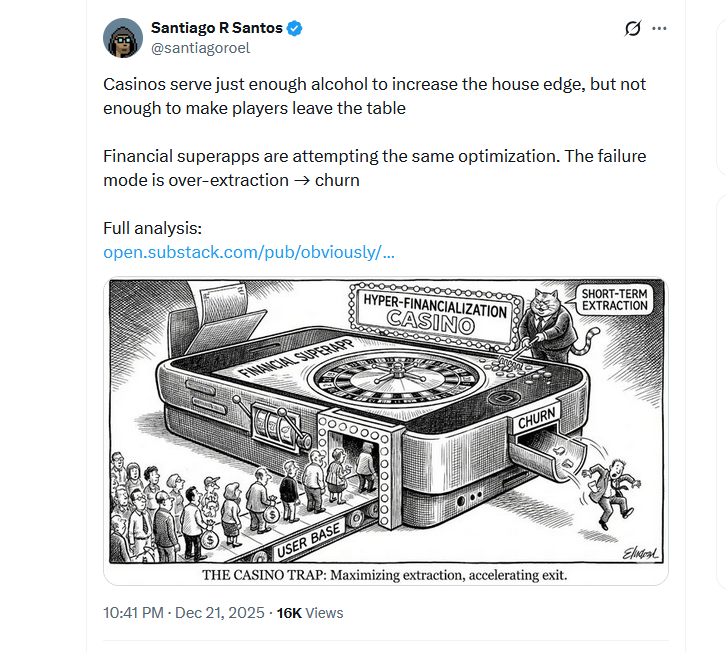

“The problem with products like casinos isn’t that users lose money; it’s that casinos accelerate customer churn,” he says.

“The longer you are in the casino, the higher the chance of liquidation. And liquidation means leaving the game completely. Users who leave have zero value.”

Robinhood is increasing its focus on prediction markets through 2025, and crypto companies Coinbase and Gemini will soon offer similar products that allow users to bet on events such as sports and politics.

Santos said these services focus too much on areas that ultimately impact the app’s primary use case. We provide easy-to-use financial services to individual customers.

“Products like Robinhood are initially successful because they are simpler, more accessible, and more digitally native than existing products,” he said.

“But users will age. Over time, the real opportunity is not to extract the most during the peak of speculation, but to grow with them and gain more economic life,” he added. “If durability is important, you need to optimize staying power.”

sauce: Santiago Roel Santos

Adoption of blockchain-based prediction markets surged amid the 2024 US elections, and Robinhood initially jumped on the bandwagon through a partnership with Kalsi in March.

Cryptocurrency exchange Coinbase announced on Wednesday that it is partnering with Calsi to add a prediction market as part of its “Everything App” push, while an affiliate of Gemini has secured a U.S. license to offer event contracts.

Ultimately, Santos believes that while prediction markets look good on balance sheets in the short term, they will become more vulnerable for financial apps later on because they pose significant risks that can destabilize users.

“Financial super apps that treat redemption as a first-class risk will ultimately strengthen their moat and improve long-term outcomes,” he argues, adding:

“If I were sitting in that seat, I would prioritize products that users naturally want as they mature financially, such as credit cards, insurance, and savings vehicles. These are boring. The data shows that that’s exactly why they work; they’re adjacent to the core relationship of managing household liquidity.”